14 |

Oilfield Technology

May

2016

known as the Central Platform. The depositional history may be

summarised as cycles of highstand carbonate deposits developing

on the shelf margins alternating with lowstand cycles of clastic

sequences thickening into the basin areas.

Numerous source rocks have been identified in this petroleum

system, including the Ordovician, Devonian Woodford, Mississippian

Barnett, Pennsylvanian, Permian Wolfcamp and Bone Springs. The

prospective stratigraphic section exceeds 10 000 ft in the Delaware

Basin, setting up thick stacked pay intervals that are now exploited

with both horizontal and vertical techniques. The most targeted

formations are Wolfcamp, Bone Spring, Avalon and Delaware Sands

and the Spraberry in the Midland Basin. Production varies from oil,

gas, and gas liquids in various zones and parts of the basin, with gas

typically increasing in occurrence at depth.

Observations

One of the relationships that can be quickly investigated is the impact

on Permian activity relative to other US basins when the price of oil

tumbled. In TGS’s production data interface, Longbow, the company

accessed permit data on a month by month basis. Figure 2 shows the

relationship of new well permits in the Permian relative to the WTI oil

price. This figure also shows Permian basin permits as a percentage

of all the US drilling permits issued.

Note both the decline in Permian permitting and the decline

in percentage of total US permitting throughout most of 2013 in

contrast to the high and increasing oil prices. With nine months

of fairly stable high prices in 2014, permitting trends upward. After

this resurgence in 2014 with a peaking of both permit count and

percentage of US total permits, followed by the steep decline in price,

remarkably, the Permian shows an upward trend in relative US permit

percentage as oil prices decline.

An anomaly can also be noted in the number of all US well

permits approved in October and November 2015. This occurred

in the state of California as operators filed an abnormal number of

permits because regulatory changes were going into effect thereafter,

which made permitting more expensive and drilling regulations more

stringent.

Figure 3 shows the map distribution of approved well permits

starting 2013 and ending March 2016.

The light blue well spots are 2013

and 2014 locations, approved

before the oil price collapse, and

the dark colours are permits issued

in 2015 and 2016. As can be seen

there is little change in the trend

or clustering of the locations of

the permits. Other than a few new

locations testing the shelf areas

and prospectivity to the southwest

in the Delaware basin, the majority

of wells are permitted in the core

of the producing areas. Where

other trends such as the Utica and

Scoop & Stack may still be expanding

geographically, Permian operators

are able to focus on sweet spots in

the multiple stacked pay areas.

Some of the more interesting

relationships are found when

working with recent production

data. In the example in Figure 4 TGS

accessed the reported measured

depth for all wells, (vertical,

directional or horizontal) and looked

at relationships of initial production

with the total drilled footage of

wells that came on production

over the 23 months before the oil

price collapse and 13 months after.

The longer the sample rate for

production the better, but because it

has a little more than a year of data

after the price collapse, the company

chose to use the initial three months

cumulative allocated production

value as a sample interval to

determine well performance.

Figure 4 plots the major component

oil from Texas production data, from

1 January, 2013 plotted against

average footage drilled per well

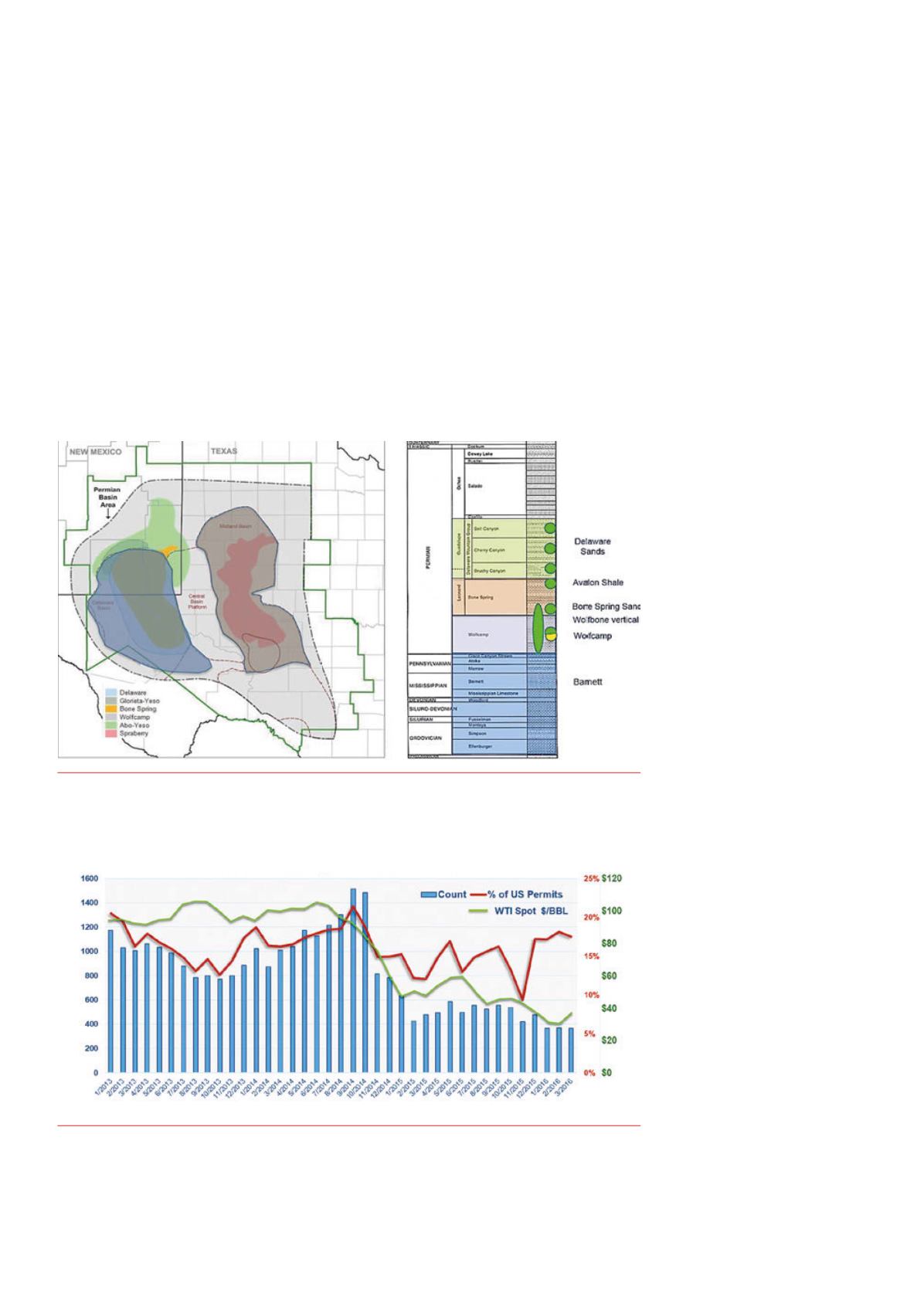

Figure 1.

PermianBasin (modified fromEIA) shadedarea illustrating theDelawareBasin inblue andMidland

Basin in grey and red. A number of prospective formations and zones are highlighted. Generalised stratigraphic

column showing commonprospective zone.

Figure 2.

Number of approvedPermianwell permits permonth from2013 through 2015 are shown on the blue

bars. The red curve shows percentage of Permianpermits to total US permits. The green curve is the spot price

of West Texas Intermediate as reportedby the EIA. Note the general increase inpercentage of Permianpermits

to total US permits as the oil price continues to sag fromJanuary 2015 to February 2016. The anomaly in%of

US permits inNovember 2015 is due to an increase inCaliforniapermits in response to regulatory changes.